Cash Flow Management for Small Businesses Guide

Let's be honest—profit on paper doesn't pay the bills. This is the first, and often harshest, lesson every small business owner learns. You can have a record-breaking sales month and still find yourself scrambling to make payroll.

This disconnect between being profitable and being cash-positive is where so many promising businesses hit a wall.

Success can even be a double-edged sword. Imagine a contractor who lands a massive project, showing a huge profit in their accounting software. Great, right? But if that client is on a 90-day payment term, the contractor still has to float payroll, buy materials, and pay rent for three months before seeing a dime. Without a healthy cash reserve, that "profitable" project could be the very thing that sinks them.

Why Cash Flow Is Your Business Lifeline

This isn't just a hypothetical problem; it's a sobering reality. An astonishing 82% of small businesses fail because of poor cash flow management. It's not about a lack of sales or a bad product—it's about running out of the actual money needed to operate day-to-day.

Even companies with steady revenue can collapse if they aren't watching their cash, a fact often highlighted by organizations like the U.S. Chamber of Commerce. You can start building good habits by reviewing these essential 5 Steps To Create Cash Flow For Your Business.

Cash flow is the oxygen for your business. You can survive for a while without profits, but you can't survive a single day without cash.

It’s the money that lets you pay your team, buy inventory, and invest in growth. Mastering it isn't just an accounting chore; it's your most powerful strategic tool. It forces you to look beyond the sales numbers and get a true picture of your company's real-time financial health.

Profit Is an Opinion, Cash Is a Fact

To get a real handle on this, you have to separate the concepts of profit and cash flow. They tell two completely different stories about your business.

Profit shows if your business model works over the long haul. It's a calculation (Revenue - Expenses) that often includes non-cash items like depreciation. It’s a great indicator, but it’s theoretical.

Cash Flow, on the other hand, is reality. It’s the actual, tangible money moving in and out of your bank account. It's what you have on hand right now to cover rent, salaries, and supplier invoices.

The table below breaks down the key distinctions.

Profit vs Cash Flow At a Glance

Concept | Profit | Cash Flow |

|---|---|---|

What it measures | Business model viability and long-term financial performance. | The company's immediate ability to pay its bills. |

Calculation | Revenue - Expenses (including non-cash items). | Cash In - Cash Out (only actual money movement). |

Timing | Measured over a period (quarterly, annually). | A real-time snapshot of liquidity. |

The "Story" It Tells | "Are we making money on paper?" | "Do we have the cash to operate today?" |

Understanding this difference is crucial. When you start managing cash proactively, you can spot potential shortfalls before they become crises, make smarter decisions, and jump on opportunities when they pop up. It’s how you shift from reactive panic to strategic, confident planning.

Create a Reliable Cash Flow Forecast

Forecasting cash flow isn't about gazing into a crystal ball. It’s about making smart, forward-looking decisions using the data you already have. Honestly, this is where most small businesses move from reactive scrambling to proactive planning. The whole point is to build a reliable picture of your financial future, week by week, so there are absolutely no surprises.

This might sound intimidating, but you don't need to be an accountant to nail it. Your most powerful tool here is the 13-week cash flow forecast.

Why 13 weeks? Because this rolling, three-month window is the sweet spot. It gives you enough detail to make immediate decisions without getting lost in long-term hypotheticals. You can anticipate payroll, plan for a big purchase, and—most importantly—spot a potential cash crunch with enough time to actually do something about it.

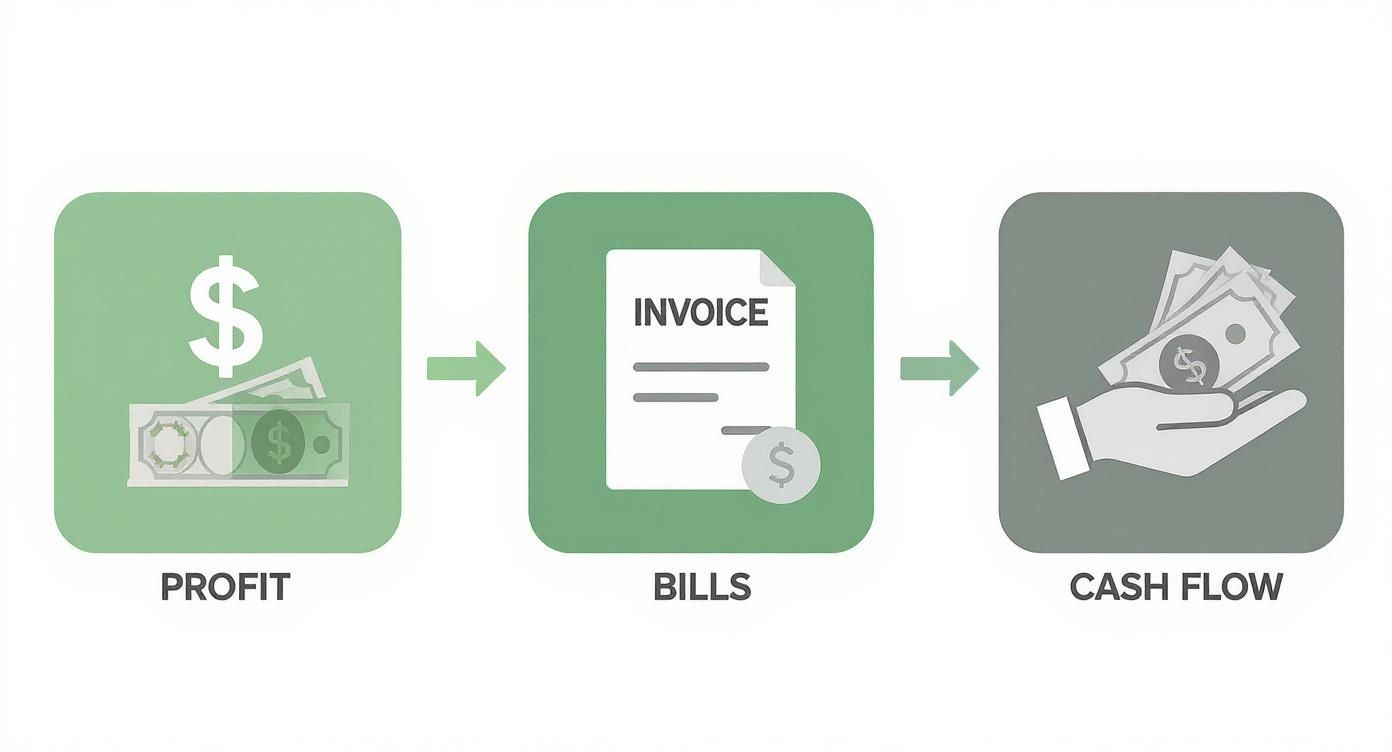

This simple visualization shows how profit must first cover your bills before it becomes positive cash flow—the essential ingredient for keeping your business alive.

As you can see, bringing in revenue is just the first step. How you manage the money going out is what really determines how much cash you have on hand.

Gathering Your Historical Data

Before you can look forward, you have to look back. Your forecast starts with collecting key financial documents from the last six to twelve months. This historical data is the foundation for spotting trends and making projections that are grounded in reality, not wishful thinking.

You'll want to pull together a few key documents:

Bank Statements: These give you the clearest, no-nonsense picture of actual cash moving in and out of your business.

Sales Records: Look for the rhythm of your business here. Are there seasonal spikes? How long does it typically take for customers to pay you?

Accounts Payable and Receivable Reports: This is your "who owes who" list. It shows money coming in (inflows) and money you owe (outflows), along with their due dates.

This information reveals the natural pulse of your business. For instance, a retail shop owner will almost certainly see a sales surge in Q4 followed by a predictable dip in Q1. Recognizing that pattern is the first step toward preparing for it. To really get this right, accurate projections are crucial. For a deeper dive, check out Your Guide to Cash Flow Projection for more detailed steps.

Projecting Your Cash Inflows

Once you have your history straight, you can start projecting the money you expect to come in over the next 13 weeks. My best advice? Be realistic, even a little conservative. It’s always better to be pleasantly surprised by extra cash than to come up short when bills are due.

Your inflows will typically come from a few sources:

Sales Revenue: Base your weekly sales projections on past performance, seasonality, and any upcoming marketing campaigns you have planned.

Customer Payments: Look at your accounts receivable. When are those outstanding invoices actually due to be paid?

Other Income: Don't forget to include any anticipated loans, investment capital, or one-off sales of assets.

For example, a consultant forecasting project-based income would map out milestone payments for each client. If a large payment is expected in week six, they can plan their expenses around that specific inflow, avoiding a cash crunch in weeks one through five.

Mapping Out Your Cash Outflows

The final piece of the puzzle is mapping out everything you expect to spend. The good news is that this side of the forecast is often more predictable than your income, since many of your expenses are fixed.

Keep things organized by breaking your outflows into a few categories:

Fixed Costs: These are your consistent, recurring expenses that don't change much. Think rent, salaries, insurance premiums, and loan repayments.

Variable Costs: These expenses fluctuate with your business activity. This includes things like inventory purchases, shipping costs, contractor payments, and your marketing budget.

One-Time Expenses: Always plan for those big, non-recurring purchases on the horizon. This could be new equipment, annual software licenses, or tax payments.

By meticulously tracking every dollar in and out, your 13-week forecast becomes a living, breathing dashboard for your business. It transforms cash flow management from a source of stress into a strategic advantage, giving you the clarity to navigate challenges and seize opportunities with confidence.

Get Paid Faster: How to Accelerate Your Cash Inflows

That gap between sending an invoice and seeing the money hit your account? It's probably one of the most stressful parts of running a business. Closing that gap is one of the most direct ways to get your cash flow in a healthier place. The good news is, you have more control over how quickly you get paid than you might think. It all starts with rethinking your approach to invoicing and payments.

Instead of just waiting for checks to arrive, you need to be proactive with your receivables. This means building a system that nudges clients to pay you on time—or even a little early. When you make this mental shift, your accounts receivable stop being a source of anxiety and become a predictable stream of income.

Modernize How You Invoice

Think of your invoice as more than just a bill. It's a tool for speeding up your cash flow. A vague, confusing, or late invoice is basically an invitation for a late payment. If you want to get paid faster, your invoicing has to be instant, clear, and professional.

This means firing off that invoice the second a job is done or a product is delivered, not waiting until the end of the month. Use simple language, itemize every charge, and make the due date and payment instructions impossible to miss. Every day you delay sending an invoice is another day you’re not getting paid.

Late payments are the number one culprit behind cash flow disruptions. The right tech can make a huge difference here. Automated billing systems, for instance, let you send invoices in real-time and see who has paid, which cuts down on delays significantly.

One analysis found that a staggering 58.7% of businesses that switched to accounts payable technology saw fewer invoicing errors. Fewer errors mean fewer questions from clients and, ultimately, faster payments.

Make It Incredibly Easy for Customers to Pay You

Often, the biggest obstacle to getting paid quickly is simple friction. If your customer has to dig up a checkbook, find an envelope, and buy a stamp, you've just added days—or even weeks—to your payment timeline. The solution is to offer modern payment options that make paying you as easy as a few clicks.

Online Payment Portals: Let clients pay you right from the invoice with a credit card, debit card, or bank transfer. This is the new standard, so if you're not doing it, you're behind.

Recurring Billing: For retainers or subscriptions, this is a game-changer. Set up automatic payments so the cash flow is guaranteed without you or your client lifting a finger.

Mobile Payments: Add options like Apple Pay or Google Pay. It’s perfect for clients who run their businesses from their phones.

By removing these small hurdles, you dramatically improve the odds of getting paid right away. This doesn't just speed up your cash cycle; it also creates a better experience for your customers. Making it easier for people to buy from you is a cornerstone of learning how to increase online sales.

Get Cash Upfront with Proactive Strategies

Beyond smarter invoicing, there are a few tactics you can use to secure cash before you even start the work. These are especially powerful for service businesses or anyone tackling large, expensive projects.

A freelance web designer, for instance, should never start building a site without a deposit. A 50% upfront payment is standard practice. It ensures you have the cash to cover your own costs and can dedicate real time to the project without financial stress.

Consider putting these policies in place:

Require Deposits: For any project over a certain size, make a 30-50% deposit mandatory. It locks in the client's commitment and gives you an immediate cash boost.

Offer Early Payment Discounts: A small incentive, like a 2% discount for paying within 10 days (known as "2/10 net 30"), can be just the push a client needs to pay your bill first.

Implement Late Payment Fees: State clearly in your contract and on every invoice that overdue payments will incur a penalty. You hope you never have to use it, but just having it there encourages people to pay on time.

These proactive steps put you back in the driver's seat of your cash flow. They aren't just one-off tricks; they're the foundational habits of a financially resilient business.

Control Cash Outflows Without Stifling Growth

Managing the money going out of your business is a real balancing act. You have to be disciplined and watch every dollar, but you also have to spend money to make money. Squeezing the budget too tight can be just as damaging as letting spending run wild—it can mean missing out on opportunities that could fuel your next big growth spurt.

The real goal isn't just to blindly "cut costs." It's about being strategic. You need a clear framework for deciding where your money goes, helping you trim the fat without cutting into the muscle of your operation. This is what separates businesses that just survive from those that truly thrive.

Get a Handle on Your Spending

First things first: you need a brutally honest look at where your money is actually going. Don't just see it as one big number leaving your bank account each month. Break it down.

A simple but powerful way to start is by splitting your expenses into two buckets:

Must-Haves: These are the non-negotiable costs to keep the lights on. Think rent, payroll for your core team, utilities, and the essential software that runs your daily operations.

Nice-to-Haves: This is everything else. It could be that new marketing campaign you're testing, extra software tools, conference travel, or that third project management app your team signed up for but barely uses.

Once you’ve sorted everything, look at the percentages. Is the "nice-to-have" category creeping up? Is one area eating up way more cash than you realized? This simple exercise almost always shines a light on some quick wins for saving cash.

Put Smart Spending Controls in Place

With a clear picture of your expenses, you can introduce some simple but effective controls. This isn't about creating corporate red tape; it's about building a culture where people think before they spend.

For example, try setting a purchase review threshold. Any new expense over, say, $500, needs a quick approval. This tiny bit of friction forces a crucial pause: "Do we really need this right now, or can it wait?" It’s a fantastic way to curb impulse buys and make sure bigger expenses actually align with your business goals.

The point isn't to micromanage every penny. It's to foster a company-wide mindset that treats cash as the precious, shared resource it is. When your team understands how their spending impacts the company's health, those small, thoughtful choices start adding up to major savings.

Talk to Your Suppliers and Optimize Your Terms

Your supplier relationships are a hidden goldmine for improving cash flow. Too many business owners just accept the initial payment terms they’re given, not realizing there’s often room to negotiate, especially if you’ve been a good customer.

Don't be afraid to have that conversation. If you're paying your invoices in 30 days (Net 30), could you ask for Net 45 or even Net 60? Pushing your payment due date out by just a few weeks can free up a surprising amount of cash, giving you more flexibility. A strong payment history is your best negotiating tool.

Also, look for chances to get better pricing. Can you get a discount by placing a larger order or consolidating your purchases with one vendor? This is especially huge for product-based businesses. Getting smart about what you buy and when is critical—you can learn more by checking out these inventory management best practices. Proactively managing your vendor relationships is one of the most underrated yet powerful tools you have.

Bridge Cash Gaps with Smart Financing

Even the most meticulously managed business can find itself in a cash crunch. It happens. A massive, unexpected order comes in that requires a huge upfront inventory purchase, or maybe a key client hits a rough patch and their payment is suddenly 30 days late. These moments don't have to be a full-blown crisis.

When you know your financing options, you can approach these gaps strategically instead of scrambling for cash at the last minute.

https://www.youtube.com/embed/yYB-_9GEpUg

The good news is that getting access to capital isn't the slow, formal ordeal it used to be. The game has changed, putting a lot more power and flexibility into the hands of small business owners who need to keep things running smoothly.

The New Landscape of Business Lending

The days of filling out mountains of paperwork and waiting weeks for a loan decision are fading fast. Fintech lenders and other alternative financing companies have completely changed the scene, offering quick applications and even faster approvals. Their speed and simplicity are a big reason why they’ve become so popular.

In fact, a recent report found that 75% of small businesses are now looking beyond traditional banks and turning to fintech or non-bank lenders. This isn't just a preference; it's often a necessity. The same report showed that 40% of businesses—even well-established ones—get turned down for traditional bank financing. This really shines a light on the need for more accessible capital, a trend you can dig into deeper by reviewing the latest small business trends report.

This doesn't mean banks are out of the picture, but it absolutely means you have more tools in your financial toolkit than ever before. The first step is figuring out what those tools are and which one is right for the job.

Key Financing Options for Your Business

Not all financing is created equal. The best choice for you depends entirely on your specific situation: why you need the money, how much you need, and how quickly you can realistically pay it back.

Let's break down some of the most common and practical options for handling short-term cash flow needs.

Business Line of Credit: Think of this as your financial safety net. It’s a revolving credit line you can tap into whenever you need it and repay over time. It’s ideal for covering unexpected bills or navigating those predictable seasonal slumps without taking on a big, lump-sum loan.

Invoice Financing (or Factoring): This is a lifesaver if your biggest headache is waiting for customers to pay. A financing company will advance you a huge chunk—often 80-90%—of your outstanding invoices. They collect the full payment from your customer later, then send you the rest, minus their fee. It's a direct way to turn your accounts receivable into cash now.

Short-Term Loans: This is the more classic option. You get a fixed amount of cash upfront and pay it back, with interest, over a set period (usually between three and 18 months). This works best for specific, one-time investments like buying a critical piece of equipment or funding a big inventory order for a guaranteed project.

Choosing the right financing is all about matching the solution to the problem. Using a short-term loan to cover daily operating costs can get expensive fast, while a line of credit probably isn't the right tool for a major capital investment.

Making the Right Choice for Your Situation

Navigating these options can seem tricky, but it really boils down to what makes the most sense for your immediate needs. Here's a quick comparison to help you weigh your choices.

Comparing Small Business Financing Options

A comparative overview of common financing solutions to help business owners choose the best fit for their cash flow needs.

Financing Type | Best For | Typical Speed | Key Consideration |

|---|---|---|---|

Business Line of Credit | Ongoing, fluctuating cash needs and unexpected expenses. | Fast (1-3 days) | Pay interest only on the amount you use. Great for flexibility. |

Invoice Financing | Businesses with long payment cycles waiting on customer invoices. | Very Fast (24-48 hours) | The cost is a percentage of the invoice value. Your customers' creditworthiness matters. |

Short-Term Loan | Specific, one-time investments like equipment or inventory. | Fast (1-5 days) | You'll have fixed, regular payments. Best for purchases with a clear ROI. |

Traditional Bank Loan | Major, long-term investments and business expansion. | Slow (Weeks to Months) | Lower interest rates but requires a strong credit history and a lengthy application. |

Ultimately, your decision should be guided by three main factors: speed, cost, and the nature of your cash flow gap. Fintech lenders are typically your fastest bet, sometimes getting you funds in 24 hours, but they might have higher rates. Traditional banks usually offer better rates, but you'll have to endure a much longer and more intense application process.

The key to smart cash flow management is to be proactive. Don't wait until your bank account is running on fumes to start exploring these options. By understanding what’s out there ahead of time, you can secure the right type of capital when you need it, turning a potential crisis into just another well-managed business decision.

Your Essential Cash Flow Management Toolkit

Putting all these strategies into practice—from forecasting to tightening up your spending—is about building a sustainable system. Financially savvy businesses don't just put out fires; they build habits that prevent them from starting in the first place. This means getting out of reactive mode and into a disciplined, proactive routine where you always have a pulse on your company's financial health.

The cornerstone of this routine is a simple weekly cash check-in. This isn't a full-blown accounting audit. It's a quick, focused look at your cash position to answer one critical question: "Are we good on cash for the next few weeks?"

Key Metrics to Track Weekly

To make these check-ins count, you need to zero in on a few numbers that give you the clearest picture. Don't get bogged down in a sea of data; start with the metrics that truly matter for survival and growth.

Cash Runway: This is your lifeline. It tells you exactly how many months your business could survive on its current cash if all revenue suddenly dried up.

Burn Rate: This is the net cash you're spending each month. Knowing your burn rate is absolutely essential for calculating and managing your cash runway.

Accounts Receivable Aging: You need to watch how long it takes customers to pay you. If invoices in the 60 or 90-day overdue columns are starting to pile up, that's a serious red flag demanding immediate attention.

Think of these metrics as your early warning system. They give you the breathing room to make smart moves before a small problem spirals into a crisis. Keeping these numbers in check is far easier when your data is centralized, which is something our guide to the best inventory management software for small business covers in depth.

Your goal is to create a rhythm where you’re always looking ahead, not just reacting to yesterday's bank balance. This consistent review transforms cash flow management from a stressful chore into a powerful strategic advantage.

Choosing the Right Tools for the Job

The right software can make this whole process practically automatic, but the trick is to find a solution that fits your business now and can grow with you later. Too many entrepreneurs fall into the trap of patching together a collection of separate apps. They might use a tool like Spocket or DSers for sourcing products and another app for invoicing, which quickly becomes a messy and inefficient setup.

While specialized tools like Autods.com or Zendrop might solve one specific problem well, they often create data silos. This fragmented approach makes it nearly impossible to get a clear, real-time snapshot of your company's overall financial health. You end up solving one problem only to create another: unnecessary complexity.

A much better approach is to start with an integrated platform built for managing your entire business. A tool like Ecommerce.co brings your sales, inventory, and financial data together into a single dashboard. This gives you a clear, holistic view of your operations from day one, helping you build a solid foundation for growth.

Got Questions? We've Got Answers

Even with the best plan in place, a few practical questions always pop up when you're in the trenches of managing your business's cash. Here are some quick answers to the ones I hear most often.

How Often Should I Be Looking at My Cash Flow Statement?

Honestly, for most small businesses, you should be checking in on your cash flow statement weekly. It's the perfect cadence. It’s frequent enough to catch a problem before it spirals but not so often that you're just staring at numbers that haven't changed.

Now, if you're in a business with super-thin margins or a lot of seasonal volatility—say, a retail shop during the holidays—a quick daily check might be smart. At the bare minimum, you absolutely must sit down for a deep dive once a month. Anything less is just flying blind.

What’s the Number One Mistake People Make with Cash Flow?

The single biggest blunder I see is confusing profit with cash. It's a classic, and it's dangerous. Your income statement can show a healthy profit, but if your clients haven't paid their invoices yet, you don't have the cash to make payroll.

A business can be wildly profitable on paper and still go under because it ran out of cash.

This cash crunch usually stems from a few culprits: customers who take forever to pay, having to buy a ton of inventory upfront, or getting blindsided by an unexpected expense. Always, always focus on having actual cash on hand to cover your immediate bills. That's more important than a big profit number on a report.

Can I Just Use a Spreadsheet to Manage All This?

Sure, you can definitely start with a spreadsheet. It’s a huge step up from not tracking your cash flow at all, and it's a great way to wrap your head around the fundamentals of money coming in and money going out.

But as your business scales, you’ll quickly hit a wall. That's when dedicated accounting software or a more integrated platform becomes a lifesaver. These tools pull in data automatically, which drastically cuts down on human error (we've all made a typo in a formula!). More importantly, they give you a live look at your finances in a way a static spreadsheet just can't match. An automated system simply makes the whole process faster and more accurate, so you can spend your time on what really matters—running your business.

Ready to stop juggling spreadsheets and get a clear, real-time view of your business's financial health? Ecommerce.co provides an all-in-one platform to manage your sales, inventory, and finances from a single dashboard. Build a solid financial foundation and make smarter decisions by visiting the Ecommerce.co website to start for free.